|

|

|

|

|

|

|

Finance | Financial advice | Immigration | Banking | Accounting | Business

By FRANCIS VAYALUMKAL

For the past few months, you might have noticed an abundance of "For Sale" signs around your neighborhood. Home sellers are plentiful, but not so many buyers. That�s not just in your neighborhood; it's becoming more the norm across the nation as existing-home prices continue to cool.

Home prices are responding to the improvements in inventory. "With the supply of homes picking up very nicely in many areas of the country, pressure is coming off of home prices," says David Lereah, chief economist of National Association of Realtors (NAR).

Even so, according to the NAR�s records, home values rose at an annual rate of 10.3 percent during the first quarter of 2006, with the median value of an existing single-family home at $217,900. During the first quarter of 2005, the median value was $197,600. The median is the point at which half of the homes sold for more and half sold for less. That 10.3 percent annual growth in the first quarter is down slightly from the 13.6 percent rate in the fourth quarter of 2005.

Many of the nation's metropolitan areas are still showing double-digit growth in home values. The NAR survey showed that 60 of the nation's 149 metropolitan regions experienced double-digit growth, while 12 regions decreased in value. Lereah expects that late summer when he reports the second quarter growth, most areas will be back in the normal rates of price growth -- single digits, not double.

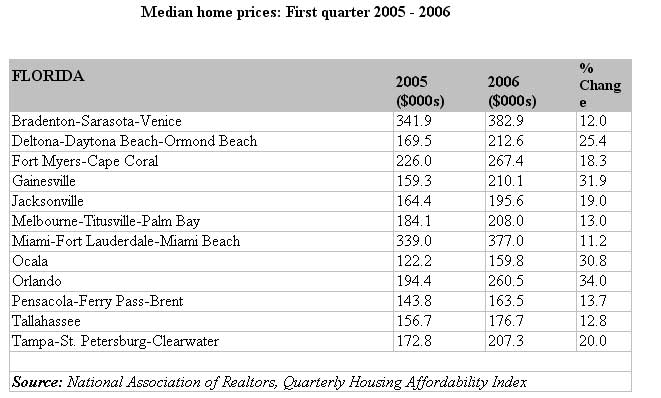

Some of the hottest regions in Florida showed marked signs of returning to those norms. The Miami metro area, for example, grew an annual 23.9 percent in the fourth quarter of 2005. The annualized growth for the first quarter of 2006 fell to 11.2 percent. In the Bradenton/Sarasota area, which grew at an annualized rate of 30 percent in the fourth quarter of 2005, the first quarter showed a much smaller 11.2 percent annualized growth rate.

The days of unbelievable growth in price are over, but homeownership is still a stable investment. "Consumers generally can expect normal price appreciation for the foreseeable future, providing solid returns over time," says Lereah.

Leading the nation in growth once again was the Phoenix-Mesa-Scottsdale area of Arizona, where the first quarter price of $268,300 is up 38.4 percent from a year ago. Florida follows with Orlando at $260,500, up 34 percent from the first quarter of 2005, and Gainesville, Fla., with a first quarter median price of $210,100, an increase of 31.9 percent in the last year.

The most expensive homes in the nation are in California. Residents of the San Jose-Sunnyvale-Santa Clara, Calif., metro area shop a housing market where the median price for an existing home is $746,800, and, in San Francisco, the price is $720,400.

The condo conversions have great effect in the market too. In certain areas of Tampa, we can see many signs advertising condominiums for sale. Most of these are condo-conversions. The availability of these condominiums added to the available home inventory. The national median condo price was $224,100 during the first quarter, which is 5.2 percent higher than a year ago. The national condo price is higher than the median single-family home because of the high concentration of condos in the most expensive metropolitan regions, says Lereah. Inventory is again a factor. The number of condos on the market has picked up more strongly than single-family homes.

"Condos have good fundamentals given the demographics of buyers, with baby boomers focused on the high end and their kids on more affordable units. However, in a handful of areas where there may be an oversupply, prices may level out, so the longer your time horizon the better your investment," says Thomas M. Stevens, president of the NAR and senior vice president of NRT Inc.

From all the numbers, we can see that the housing market is cooling off. But that doesn�t mean a real estate bust. As Lereah says, "We now see appreciation cooling to single-digit rates of growth � another sign that the markets are stabilizing.�

Finance | Financial advice | Immigration | Banking | Accounting | Business

By NITESH PATEL

Today, the average American can expect to live a record 77.6 years, according to the Centers for Disease Control and Prevention's National Center for Health Statistics, with women outliving men by an average of 5.3 years. (Centers for Disease Control, Feb. 28, 2005) Many of us carry life insurance to protect our families and assets in case of premature death. But what about disability insurance coverage? Your odds of having a disabling disease or injury before you retire are significantly higher than your premature death.

Nearly 1 person in 4 between the ages of 25 to 65 will suffer a disability lasting at least 90 days during their working career, according to a widely used industry standard called the 1985 Commissioner's Individual Disability Table. And, if you�re 35 or 40, you still face 25 to 30 years or more before you qualify for retirement benefits.

Despite those odds, surprisingly few people have adequate disability insurance protection.

If you suddenly became disabled for months or even years, your ability to pay your bills would be seriously jeopardized. Whether you have dependents or are single, or whether you have a salaried job or are self-employed, disability income insurance is one of the most important coverages you can buy.

What should you look for in a disability insurance policy? Most experts agree you'll need at least 60 percent of your gross income for as long as you can't work. Why just 60 percent? Most people pay their disability premiums with after-tax dollars, so any benefits they receive are tax-free.

Here are some options to look for:

Loss of income � Look for a policy that pays if you lose income due to disability. Some policies pay benefits only if you are totally disabled and cannot work.

Transition Benefits � Another smart option is transition benefits that help cover your financial loss even though you're no longer disabled. Assume you are self-employed and suffer a

heart attack. Eight months later, you return to work, but your income is down 30 percent because some customers have gone elsewhere. Under a policy that pays a benefit proportionate to your loss of income, you'll receive 30 percent of your benefit.

Partial Disability � Partial disability protection allows you to return to work part time and still collect benefits. This protects you if you develop a degenerative disease that leads to partial disability and progresses into total disability.

Inflation Rider � An inflation rider increases your monthly benefit as the cost of living rises (usually determined by the Consumer Price Index). In addition, look for future insurability, which allows you to increase your coverage regardless of changes in your health, activities or occupation.

The most comprehensive policies are non-cancelable and guaranteed renewable. This means the insurance company can't refuse to renew your policy if your health fails, and it can't raise your premium until age 65.

Once you've decided which type of policy you need, consider two other features that can affect your costs:

Beginning date � This is the length of time, or delay period, you're willing to wait until benefit payments begin. Most professionals recommend a 90-day period, under which benefit payments begin four months after the onset of disability � the 90-day delay period, plus 30 days for the insurer to issue the first check. By living off savings for four months, you can significantly reduce the cost of your disability policy.

Maximum benefit period � This refers to how long you will receive benefits. Policies may pay benefits for one, two or five years, until you reach age 65, or you may extend the benefit

period to age 70. Most policyholders choose age 65, when retirement and pension income typically become effective.

Group Policies � Know the Limitations

Because disability insurance can be expensive, many people purchase group policies through their employers. Although these typically cost less than individual policies, they often provide less comprehensive coverage. And, as the group ages, the insurance company reserves the right to either raise premiums � and employers often pass these increases on to employees � or cancel coverage altogether.

Moreover, many group policies exclude certain disabilities, and benefit periods may expire. If you're covered by a group plan offered though a company or office, that coverage typically ends if you resign, unlike an individual policy that remains with you regardless of your employer.

Because of those limitations, you might choose to carry an individual policy. A number of premium options are available. Some are a flat rate that remains the same for as long as you own the contract. Others increase over the duration of the policy, and a third type � favored by many young professionals � is annually renewable and may be converted to a flat rate. Your best bet is to talk with a financial professional who can help you assess the coverage that�s best for you.

Whether you buy individual disability income insurance as your sole protection against disability or as a supplement to your group coverage, the important thing is to make sure you're covered.

2 2003-2004 JHA, Inc. Disability Fact Book

Nitesh Patel is a financial representative with the Northwestern Mutual Financial Network based in Clearwater for The Northwestern Mutual Life Insurance Company, Milwaukee, Wisconsin). To reach Patel, call (727) 799-3007 or e-mail [email protected].

Finance | Financial advice | Immigration | Banking | Accounting | Business

By Dr. RAM P. RAMCHARRAN

Special Needs Trusts (SNTs) play a significant role in planning for the future of a child with a serious disability. Because SNT assets are owned by the trust, rather than the beneficiary, an SNT enables a family to provide supplemental funds to enhance a child�s lifestyle without jeopardizing eligibility for government benefits. The SNT trustee has discretionary responsibility for distributing SNT funds to pay for goods and services and ensuring that distributions are never made directly to the beneficiary.

To retain the benefits of a trust, you must have the trust structured correctly. If you have not done so already, find an attorney with experience and expertise in this area. This is a highly special area, so don�t use your real estate attorney. If you are not careful all the planning and saving you have done can go to waste. The attorney can draft the appropriate trust documentation and provide accurate, up-to-date advice and guidance. If you need to locate SNT attorney in your local area, visit www.specialneedsalliance.com or www.naela.org. These two web site are excellent tools to find a professional to meet your need.

SNT TRUSTEE OPTIONS

One of the most critical decisions related to establishing an SNT is deciding who will act as trustee. All families should be aware of the following alternatives:

* Hiring an individual professional trustee. You can use a Trustee/Service Provider Referral Program to help find SNT attorneys or non-profit organizations that serve as SNT trustees.

* Serving as trustees yourself, possibly naming a professional as co-trustee or successor trustee.

* If eligible, utilizing a bank or brokerage trust company as agent to be trustee. An agent assists in trust administration and other financial services related to the trust. Trust Companies can assume a role of trustee but some may have minimum assets for them to serve as a trustee.

TRUST PROTECTORS AND TRUST ADVISORY COMMITTEES

�A family member who chooses to retain a professional SNT trustee may opt to remain involved in the oversight of the trust by becoming a Trust Protector. This non-fiduciary role has no set responsibilities or powers but often encompasses the authority to appoint or remove trustees and investment advisors, make administrative changes to the trust document or even move the trust to a new jurisdiction. Essentially, the Trust Protector role allows a concerned family member to monitor the trustee's actions, to ensure they are consistent with the intent of the trust, while not assuming the legal liability exposure of the trustee.�

WHAT YOU SHOULD KNOW ABOUT ASSUMING THE TRUSTEE ROLE

At least 90 percent of families choose to assume the role of SNT trustee, believing they are better able to meet the needs of their loved ones rather than outside professionals. Families also choose this option when they cannot meet the $1/2 million-plus minimums that most large banks require to serve as corporate trustees.

If you decided to assume the trustee role, I suggest that you discuss the issue thoroughly with the SNT attorney. I also recommend that you purchase an informative book, the Special Needs Trust Administration Manual: A Guide for Trustees, written by a team of SNT attorneys and approved by the Office of the General Counsel for distribution. The book, which can be purchased at http://www.disabilitiesbooks.com, covers a wide range of issues, including:

* The role of government benefits such as Supplemental Security Income and Social Security Disability Income.

* Fiduciary responsibilities related to investment of trust assets.

* Handling of trust disbursements.

* Trust recordkeeping requirements.

In speaking with families about their decision to serve as SNT trustee, I am reminded of the complexity of this responsibility and the critical importance of following all guidelines accurately to avoid jeopardizing a child�s government benefits. Listed below is a checklist of SNT trustee responsibilities:

* Understanding the beneficiary�s situation and needs.

* Becoming familiar with the language and intent of the trust document.

* Obtaining IRS tax registration for the trust.

* Receiving and conducting an inventory of trust assets.

* Hiring and regularly monitoring agents and service providers.

* Arranging for the safekeeping and security of trust assets.

* Establishing accounts for management of trust assets.

* Collecting income and prudently managing investment assets.

* Maintaining records for all income and principal transactions and preparing periodic accountings.

* Preparing and filing annual federal and state fiduciary income tax returns.

* Monitoring all disbursements to help ensure maintenance of any benefit entitlements. s

* Maintaining communication with the beneficiary and all service providers.

Planning for a Special Needs person is extremely complexed and must be taken seriously. If you have not sought the advice of a professional, I would urge you to make the effort now because the longer you wait you are just asking for trouble.

Dr. Ram P. Ramcharran can be reached at [email protected]

Finance | Financial advice | Immigration | Banking | Accounting | Business

By KAMLESH H. PATEL, CPA

Every year, thousands of taxpayers are misled into believing tax schemes that are too good to be true. Falling for these scams will cost you money and may subject you to civil and criminal tax penalties. The IRS has released the 2006 list of current tax scams, which it calls the �dirty dozen.�

1. �Phishing.� Criminals work through the Internet posing as IRS representatives. They trick taxpayers into revealing their personal financial information to steal from them.

2. Zero wages. The taxpayer fraudulently disputes income information submitted to the IRS on W-2s, 1099s, etc.

3. Form 843 tax abatement. In this scam, the taxpayer requests abatement of previously paid taxes using Form 843.

4. Zero return. Promoters of this scam tell taxpayers to enter all zeros on their tax returns.

5. Trust misuse. Promoters tell taxpayers that transferring assets into trusts will reduce or eliminate their taxes.

6. Frivolous arguments. Ads suggest that paying taxes is voluntary and try to sell taxpayers �untax packages.�

7. Preparer fraud. If a tax-cutting scheme sounds too good to be true, it probably is. Taxpayers are reminded that they, not an unscrupulous preparer, are ultimately responsible for the accuracy of their returns.

8. Credit counseling agencies. Agencies claim they can fix credit ratings and aggressively push debt payment plans while imposing high fees that just add to the taxpayer�s existing debt.

9. Charitable organization fraud. Tax-exempt organizations are improperly used to shield income or assets from tax.

10. Offshore transactions. Offshore credit cards, trusts, or other arrangements are used to hide income or claim false deductions.

11. Employment tax evasion. Employers are misled into believing that they aren�t required to withhold taxes from employees� wages.

12. No gain deduction. Taxpayers are told they can eliminate their entire income by taking a �no gain realized� deduction.

use an IRA to save for retirement

Are you saving enough for a comfortable retirement? You can no longer rely on Social Security or a company pension to provide all the retirement income you will need. Perhaps, it�s time you considered an individual retirement account (IRA) as another option for setting aside more retirement dollars. Consider these basic IRA facts.

Deductible IRA. If you are not covered by an employer�s retirement plan, you may contribute up to $4,000 to a traditional deductible IRA for 2006 ($5,000 if you�re 50 or older). If you�re covered by a company plan, the amount you may contribute begins to phase out once your adjusted gross income (AGI) exceeds $50,000 (single) or $75,000 (married filing jointly). If you�re not covered by a company plan, but your spouse is, the phase-out income range is $150,000 to $160,000. If you qualify, your IRA contribution is tax-deductible, and taxes on earnings and gains are deferred until you start taking withdrawals. This allows a tax-free compounding of earnings and gains. The IRS imposes timing restrictions on withdrawals; they must begin after age 70�, and they�re generally subject to a 10 percent penalty if taken before age 59�.

Roth IRA. A married couple with income of less than $160,000 or a single person with income of less than $110,000 may be eligible to open a Roth IRA. As you approach these levels, the IRS limits the amount of a Roth contribution you can make. Annual contribution limits are the same as for a traditional IRA, but contributions are not tax-deductible. Once you�ve had the Roth account for five years and you�re at least 59�, your withdrawals are completely tax-free.

Nondeductible IRA. What if you don�t qualify for either a deductible IRA or a Roth? You might consider a nondeductible IRA. Though the contribution isn�t deductible, the taxes on the earnings and gains are deferred until you take withdrawals.

planning a move? don�t forget taxes

Millions of people move each year, often during the summer months when children are out of school. If you�re considering a move this summer, be aware that moving can have some important tax consequences.

Retirement plans. If you have a retirement plan at work, you may have several choices upon leaving a job. You can roll your retirement funds into an IRA, possibly roll the money into a new employer�s plan, or perhaps even leave the money in your former employer�s plan. Keep in mind that any amount distributed directly to you is subject to automatic 20 percent income tax withholding, and you may also face a 10 percent early withdrawal penalty.

401(k) loans. Facing a layoff or new job and need cash? Tap your 401(k) balance only as a last resort. If you have an existing 401(k) loan, pay it off. If you leave your employer and can�t repay the loan within a preset time, the loan balance is considered a withdrawal. As such, you�ll be hit with income taxes and possibly a 10 percent penalty.

Job search expenses. Expenses incurred to search for a new job are tax-deductible, even if your job search doesn�t land you that coveted position. To qualify, you must be looking for a job in the same occupation.

Moving expenses. If your job-related move qualifies (the IRS has both a distance and a time test), you can deduct the costs of moving your household goods and your family.

Home sale. When you sell your home, you can exclude up to $250,000 of the gain from your taxes. The exclusion amount is $500,000 for married couples filing a joint return. To qualify for the full exclusion, you must have owned and occupied the house as your main home for two out of the five years prior to its sale. A partial exclusion may apply if you fail the two-year test due to a job-related move.

Kamlesh H. Patel, CPA, can be reached at (813) 289-5512 or (813) 846-5687 or e-mail [email protected] or [email protected].

Finance | Financial advice | Immigration | Banking | Accounting | Business

By BRIAN STEPHENS

Many factors affect the value of a business but ultimately the buyer has to be convinced that the business is worth the investment dollars. But the total dollars earned by a business accounts for only part of the reason buyers invest in buying businesses.

Empire Business Brokers� unique benchmark analysis considers nearly 84 factors that influence a business� ability to fetch a great price. Over the next few columns, we will highlight 15 core benchmarks that business owners should consider if they plan to eventually sell their businesses someday. Many of the benchmarks are best focused on a year or more before the owner wants to sell. Buyers also should consider these factors when looking for a great investment. Here are the first three:

1. SHOW IT ALL: Since most businesses sell for a multiple of their total bottom-line profit, it is important to show every penny as recorded income. Even the tax savings from unreported earning earnings does offset the value of reporting every penny.

Assume a business owner saves 40 percent in taxes on a $1,000 of �unreported� earnings; the owner saves $400 in taxes each year he or she for failing to report the $1,000. But a good business can easily sell for 2.5 times the bottom-line earnings, which means the owner looses $2,500 when it comes time to sell.

2. REACH FOR THE SKY: Keep the sales trend up or at least flat. Often times, owners will approach the last few years of owning a business with a more relax approach, cutting back on staff or becoming more relaxed about marketing.

Often it is after sales take their natural decline that the owners then begin searching for a buyer. The problem is that buyers see the decline in sales as a reflection of the business. As a result of the decline in sales, the buyer puts a big discount on the business� value. And while the seller may be able to explain why the sales declined and how �easy� it will be to bring sales up, the buyer continues to think the business is far less valuable than if the sales were up or at least relatively flat.

3. YOU CAN�T TAKE IT WITH YOU: Each business has a signature of genius within. It is that very same genius that makes it different from each other businesses. It also is what makes a particular business successful over its competitors. Therefore, that unique genius adds incredible value to the business -- but only if the buyer can grasp that genius for himself or herself.

If that incredible way of operating disappears when the owner leaves, the business is hardly worth much more than the value of the used equipment. Creating an operating manual can help transfer those unique operating features to the new business owner. One can start with a simple notebook to record ideas and process. Over a few months, one should have enough tips and ideas to begin a great operations manual.

In the end, we suggest following the Golden Rule that reminds sellers to stand in the shoes of the buyer. Can you see all the sales? Is the business holding on to its position against its competition? Can the buyer run this business just like the previous owner? We will consider more factors of influence in our next article.

Brian Stephens of Empire Business Brokers in Tampa can be reached at 813 571-7700 or via e-mail at [email protected].

|

|

Contact Information

Anything that appears in Khaas Baat cannot be reproduced, whether wholly or in part, without permission. Opinions expressed by Khaas Baat contributors are their own and do not reflect the publisher's opinion.

The Editor: [email protected] Advertising: [email protected] Webmaster: [email protected] Send mail to [email protected] with questions or comments about this web site. Copyright � 2004 Khaas Baat.

Khaas Baat reserves the right to edit and/or reject any advertising. Khaas Baat is not responsible for errors in advertising or for the validity of any claims made by its advertisers. Khaas Baat is published by Khaas Baat Communications.

|

Francis Vayalumkal is a loan officer at Market Street Mortgage and can be reached at (813) 971-7555 or via e-mail at

Francis Vayalumkal is a loan officer at Market Street Mortgage and can be reached at (813) 971-7555 or via e-mail at